Europe’s Economic Geography

Anupam Bapat, reporting from the United Nations Economic Commission for Europe (UNECE), talks about the history of Europe and how it can make a difference in maintaining the economic and social relations amongst the neighboring states.

History illustrates that Europe is a dynamic and evolving entity with multiple faces, identities, expressions, experiences, and diversified cooperation forms. It is a two-thousand-year old civilization with a multiplicity of cultures. It is also a socio-economic model with a unique integration process. European history is characterized by forms and attempts of economic, political, military, and cultural cooperation to search for the equilibrium between integration and diversity within certain contours. The variety in ethnicity could be considered one of the factors which could influence the type of culture emerging, but disregarding the all the points, a complex, yet composite agenda can be made which all the nations could agree upon.

An example of a country having a very eventful history is the United Kingdom. In the 1800’s, a group of islands agreed to come together to form the United Kingdom. They began hostilities against the Germans in the First World War (1914), which was fought in the grueling trenches of Belgium and France. Declaring war against the Germans in a similar situation was Italy. Therefore, the point of focus is that having a similar history makes the nations relate to the problems regarding the economies.

The concept of European identity was introduced for the first time in the European political agenda with the “Declaration on European Identity” in Copenhagen on 14 December 1973. It was said that cooperation among European peoples represents a real need to effectively face the current global threats [1]. The diversity in the population can also be a positive aspect to the main role to be played.

The first attempt to push European integration beyond the notion of a common market dates back to 1976 with the Tindemans Report [2]. In that report, there is a chapter dedicated to the rise in awareness of being a European by increasing the symbolic representations of unity amongst the nations where the Christian culture plays a huge part in growing a sense of unity amongst the European citizens. A common flag and national anthem for Europeans also helped them unite and ignited a sense of brotherhood. The evolution of the European identity issue within the major European Treaties highlights the fact that the importance of political legitimization of the European Union (EU) institutions was clearly perceived only in the eighties.

A milestone in the European integration process was represented by the Treaty of Maastricht (1993). It instituted the establishment of a “European citizenship,” a legal status which guarantees a set of rights to the individuals possessing the nationality of one of the member states. These ideas and treaties are a good opportunity for the citizens and the government officials of various countries to come closer and be more impactful.

In short, there are various ways to imply that the sense of togetherness should be there amongst the European citizens and the government officials and these ways should be elaborated and introduced to all the citizens in order to make sure that there is a sense of peace amongst all.

(Edited by Harsha Sista.)

Who Will Clean Up the Mess?

Nivedan Vishwanath, reporting from the United Nations Economic Commission for Europe (UNECE), explores the role of the United Nations (UN) in the Eurozone crisis.

The International Monetary Fund (IMF) has played a major role in the Eurozone crisis. Despite being independent, the IMF is still recognised as a part of the United Nations (UN) system and it is the only institution through which the UN has impacted the crisis. The role that the UN played was discussed along with an analysis of other institutions like the European Central Bank (ECB) and the European Commission (EC). The EC and the ECB received heavy criticism with respect to their modus operandi. The Eurozone is largely dependent on the IMF for bailouts and several other loans. While central banks in other countries (for example: Japan) stand behind their sovereign debt and serve as a last resort before approaching the IMF, a lack of the same was observed in the Eurozone. A structure like this is quintessential in the Eurozone. Another point that was deliberated upon was the flow of cash and other assets over borders. All the delegates agreed to the fact that the systems responsible to monitor these flow channels are inefficient and upgradation of these systems will be instrumental in taking down transactions similar to the one between the Hellenic State (Greece) and Goldman Sachs.

Several remedial measures were brought up for discussion. Suggestions to establish the European Systemic Risk Board (ESRB) to monitor and tackle private credit (and real estate) bubbles across the zone were made. The one major flaw that exists within the ECB is that it fails to take into account the member states’ models of growth and competitiveness during the policy-making process. The European Union (EU) as a whole needs to find a flexible approach to economic governance and take into account the differences in the functioning of member state governments. A suggestion was made to appoint the Bank of International Settlements (BIS) as the reviewing body for all ECB policy decisions. All these highlight that an improvement in economic integration among Eurozone member states is required and proper monitoring and reviewing mechanisms for various cash flow channels and policy decisions should be established.

(Edited by Harsha Sista.)

The Lehman Brothers Scandal And Its Effects On The European Union

Anupam Bapat, reporting from the United Nations Economic Commission for Europe (UNECE), analyses the effects and the outcomes of the Lehman Brothers Scandal.

Lehman Brothers Holding Incorporation was a global financial services firm which fourth-largest investment bank in the United States of America (USA), behind Goldman Sachs, Morgan Stanley, and Merrill Lynch. Founded in the 1850’s and running for 158 years, it was doing business in investment banking, equity, and fixed-income sales and trading. Fuld, the then Chief Executive Officer (CEO), had steered Lehman through the 1997 Asian Financial Crisis, a period where the firm's share price dropped to $22 USD in 1998, but he was said to have underestimated the downturn in the US housing market and its effect on Lehman's mortgage bond underwriting business.

While there may have been several reasons for the firm's ultimate failure, it was caused in large part by the housing crisis in 2008. The firm survived many of the world's largest disasters, including two World Wars and the Great Depression. However, it was its over-leveraging and unwieldy venture into subprime lending that caused its ultimate downfall. This kind of scandal was one of the causes of the economic disaster in the USA and the European Union as a whole. Over an estimated 6 million jobs were lost, unemployment rose 10%, the Dow Jones Industrial Average (DOW) dropped an astounding 5,000 points, according to ABC News. The international ripple effect also devastated economies like Latvia, Hungary, and Lithuania (not to mention the European Union).

A state of depression was felt by different nations and they sought help from various financial institutions like the International Monetary Fund (IMF), the World Bank (WB) and the European Central Bank (ECB). Countries like Greece, Iceland and Pakistan were more than just devastated. Trust remained an enormous question mark following Lehman's collapse. The public, which had previously placed so much trust (and money) into "too big to fail" firms like Lehman, were suddenly finding themselves skeptical of the economy altogether. Lehman's example proved a turning point in finance to a historic degree.

For many, the economy is steadily flowing toward another financial crisis–an example being the warning signs of Lehman. The global economy currently has a $237 trillion total debt—some $70 trillion higher than before the Lehman Brothers collapsed, according to the Financial Times. Additionally, concerns over monetary policy and quantitative easing, as well as back-to-back negative Gross Domestic Product (GDP) growth could contribute to another recession. To conclude, by proper analysis, the world can evade another Lehman Brothers Scandal and be safe from another recession.

(Edited by Harsha Sista.)

All That Matters, In The End, Is Money

Nivedan Vishwanath, reporting from the United Nations Economic Commission for Europe (UNECE), analyses the possible reforms in the European banking sector.

In the end, it all comes down to money. A proper monetary framework is key for any region to progress. Until and unless the Eurozone improves its monetary framework and introduces reforms in the banking sector, a proper recovery from the economic crisis can be knotty. The crisis for the Eurozone started when the dubious transaction between Greece and Goldman Sachs was carried out. By the time the consequences of this transaction were realised, the situation had spiraled out of control and eventually led to Greece announcing its € 300bn debt in 2010. While a lot can be done to reform the banking sector and pull the zone out of the crisis, a large number of the member states are counting on Quantitative Easing (QE) and deposit insurances as the possible reform options.

Under QE, central banks create money to buy financial assets. These purchases increase the demand for these assets and subsequently, bring the yield down. When this happens, individuals and corporates are encouraged to buy them and also, spend them. This expenditure eventually leads to job creation and drives economic growth. This ensures that two birds are killed with one stone—unemployment goes down and the economy grows. On introducing QE in the economic framework of the Eurozone, the Economic Central Bank (ECB) will be able to buy asset-backed securities. In the event of an inflation deterioration in the Eurozone, QE can be implemented as a full asset purchase program. With QE in place, one can hope for an increase in the manufacturing index as well as overall export activities.

Along with QE, the introduction of sovereign concentration charges for banks and common deposit insurance should also take place. Not only this, but a tighter treatment of Non-Performing Loans (NPLs) should also be ensured. Governments usually force domestic banks to grant them preferential credit conditions by using access to the funds that come through individual deposits. The above-introduced measures ensure that the government does not abuse the system. In order to implement these measures, a full replacement of the existing system was suggested. The new system would be a single Euro area Deposit Insurance Scheme (DIS). The idea of DIS was sided by a majority of the member states because of several inefficiencies in the present system. These states believe that this new system could gradually bring everything back on track.

(Edited by Harsha Sista.)

Hope is around the corner

Nivedan Vishwanath, reporting from the United Nations Economic Commission for Europe (UNECE), analyses alternative measures to handle the Eurozone crisis.

Premise: The Eurozone wants to promote growth and it has been left with only two choices—impose austerity measures and consolidate all finances, or accommodate monetary policies and introduce quantitative easing. While the former can suspend growth and push recovering economies into recession, the latter option is expected to provide a more flexible approach to economic governance. This has been considered necessary because the European Union (EU) has failed to take into account the differences in the way in which the governments of member states operate.

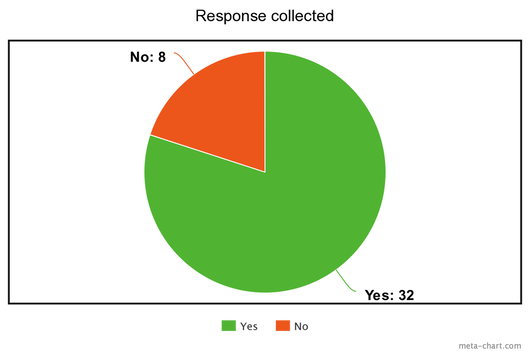

Question: Does the committee believe that a continued accommodation of the monetary policy and modest inflation on a long-term basis ensure improvement in Eurozone’s condition?

Sample Space: Albania, Austria, Belgium, Germany, International Monetary Fund (IMF), European Central Bank (ECB), Netherlands, Estonia, Liechtenstein, Ireland, Greece, World Bank, Switzerland, Bulgaria, Monaco, Czech Republic, Cyprus, Ukraine, Romania, Hungary, Slovenia, European Commission (EC), Finland, Slovakia, Serbia, Lithuania, United States of America (USA), Iceland, Poland, Portugal, Latvia, Bosnia, Goldman Sachs, Azerbaijan, France, Russia, Denmark, Spain, Turkey, United Kingdom (UK).

Response: 32 of the 40 countries and organisations voted YES, while 8 voted NO. The IMF, World Bank and the ECB voted YES.

Inference: A large majority of the sample space believes that this new approach is better than enforcing austerity measures. They believe that this approach will ensure better results. However, there are countries which believe that imposing austerity measures will actually prevent dwindling economies from defaulting.

(Edited by Harsha Sista.)

Question: Does the committee believe that a continued accommodation of the monetary policy and modest inflation on a long-term basis ensure improvement in Eurozone’s condition?

Sample Space: Albania, Austria, Belgium, Germany, International Monetary Fund (IMF), European Central Bank (ECB), Netherlands, Estonia, Liechtenstein, Ireland, Greece, World Bank, Switzerland, Bulgaria, Monaco, Czech Republic, Cyprus, Ukraine, Romania, Hungary, Slovenia, European Commission (EC), Finland, Slovakia, Serbia, Lithuania, United States of America (USA), Iceland, Poland, Portugal, Latvia, Bosnia, Goldman Sachs, Azerbaijan, France, Russia, Denmark, Spain, Turkey, United Kingdom (UK).

Response: 32 of the 40 countries and organisations voted YES, while 8 voted NO. The IMF, World Bank and the ECB voted YES.

Inference: A large majority of the sample space believes that this new approach is better than enforcing austerity measures. They believe that this approach will ensure better results. However, there are countries which believe that imposing austerity measures will actually prevent dwindling economies from defaulting.

(Edited by Harsha Sista.)